- 歐洲央行決議維持利率不變,歐元區三大主要利率分別是隔夜存款利率為4%,主要再融資利率(MRO)為4.5%、隔夜貸款利率(MLF)為4.75%

- 歐洲央行下調通膨預期,主因反映能源價格下跌,預估2024年平均通膨率為2.3%(下修0.4%),2025年為2%(下修0.1%),2026年會進一步縮減到1.9%(沒變)

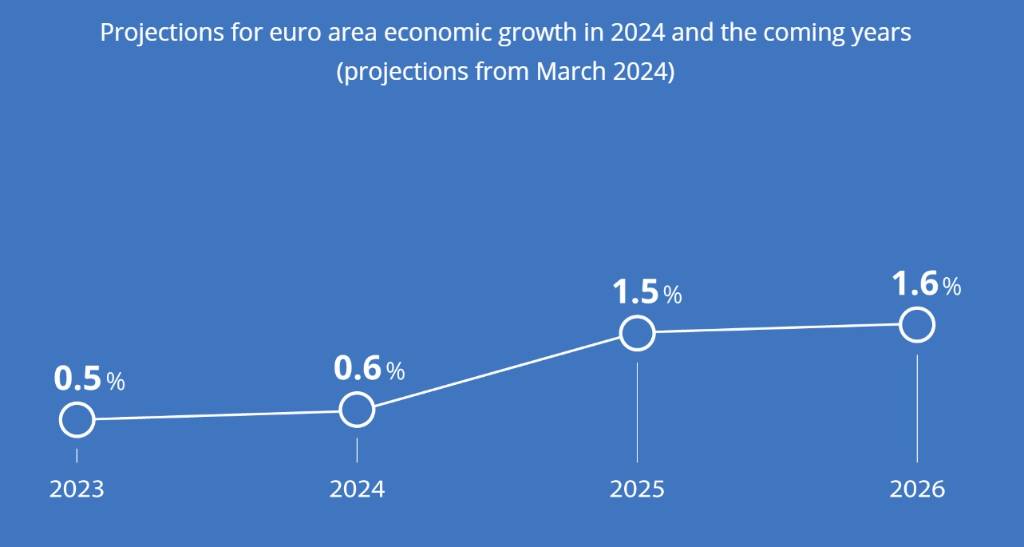

- 歐元區2024年經濟成長率預估調降到0.6%(下修0.2%),之後因消費與投資支撐,2025年經濟成長率會上升到1.5%(沒變),2026年為1.6%(上修0.1%)

歐洲央行3月7日召開決策會議,決議維持利率不變,歐元區三大主要利率分別是隔夜存款利率為4%,主要再融資利率(MRO)為4.5%、隔夜貸款利率(MLF)為4.75%,仍然是1999年歐元問世以來新高。

回顧ECB自2022年7月21日升息2碼開始啟動本波升息循環,至2023年9月14日共計升息10次,宣布時間依序為2022年7月21日升息2碼,2022年9月5日升息3碼,2022年10月27日升息3碼,2022年12月15日升息2碼,2023年2月2日升息2碼,2023年3月16日升息2碼,2023年5月4日升息1碼,2023年6月15日升息1碼,2023年7月27日升息1碼,以及2023年9月14日升息1碼,2022年共計升息4次,累計升幅為10碼(2.5%),2023年升息6次,升幅為8碼(2%),合計升幅18碼(4.5%)。

歐洲央行下調通膨預期,主因反映能源價格下跌,預估2024年平均通膨率為2.3%(較2023年12月14日的預估值縮減0.4%),2025年為2%(較2023年12月14日的預估值縮減0.1%),2026年會進一步縮減到1.9%(沒變)。不含能源與食物後的核心通膨率預估值也下調,預估2024年核心通膨率為2.6%(較2023年12月14日的預估值縮減0.1%),2025年為2.1%(較2023年12月14日的預估值縮減0.2%),2026年會再縮減到2%(較2023年12月14日的預估值縮減0.1%)。

儘管多數潛在通膨指標已經進一步緩解,但歐元區物價壓力還是很高,部分原因來自於薪資強勁成長。融資受到高利率限制,累計的升息持續對需求構成壓力。歐元區經濟成長率預估值下修,2024年經濟成長率預估調降到0.6%(較2023年12月14日的預估值下修0.2%),之後因消費與投資支撐,2025年經濟成長率會上升到1.5%(沒變),2026年為1.6%(較2023年12月14日的預估值上修0.1%)。

委員會決心確保通膨及時回到2%的中期目標,根據目前評估,若歐洲央行利率維持足夠長的時間,將會為此目標做出重大貢獻。

關於先前購債(QE)後的縮減資產負債表(縮表/QT)行動,原先常態性的資產購買計畫(APP)所有購入的有價證券,到期後回收的本金不再進行投資,APP投資組合正在以可預測的速度下降中。針對疫情的緊急購債計畫(PEPP),2024年上半年維持所有購入的有價證券到期本金全數再投資,2024年下半年PEPP投資組合每月計畫減少75億歐元,2024年底之後所有有價證券到期本金停止再投資。

7 March 2024

The Governing Council today decided to keep the three key ECB interest rates unchanged. Since the last Governing Council meeting in January, inflation has declined further. In the latest ECB staff projections, inflation has been revised down, in particular for 2024 which mainly reflects a lower contribution from energy prices. Staff now project inflation to average 2.3% in 2024, 2.0% in 2025 and 1.9% in 2026. The projections for inflation excluding energy and food have also been revised down and average 2.6% for 2024, 2.1% for 2025 and 2.0% for 2026. Although most measures of underlying inflation have eased further, domestic price pressures remain high, in part owing to strong growth in wages. Financing conditions are restrictive and the past interest rate increases continue to weigh on demand, which is helping push down inflation. Staff have revised down their growth projection for 2024 to 0.6%, with economic activity expected to remain subdued in the near term. Thereafter, staff expect the economy to pick up and to grow at 1.5% in 2025 and 1.6% in 2026, supported initially by consumption and later also by investment.

The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. Based on its current assessment, the Governing Council considers that the key ECB interest rates are at levels that, maintained for a sufficiently long duration, will make a substantial contribution to this goal. The Governing Council’s future decisions will ensure that policy rates will be set at sufficiently restrictive levels for as long as necessary.

The Governing Council will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction. In particular, the Governing Council’s interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission.

Key ECB interest rates

The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 4.50%, 4.75% and 4.00% respectively.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP portfolio is declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

The Governing Council intends to continue to reinvest, in full, the principal payments from maturing securities purchased under the PEPP during the first half of 2024. Over the second half of the year, it intends to reduce the PEPP portfolio by €7.5 billion per month on average. The Governing Council intends to discontinue reinvestments under the PEPP at the end of 2024.

The Governing Council will continue applying flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to countering risks to the monetary policy transmission mechanism related to the pandemic.

Refinancing operations

As banks are repaying the amounts borrowed under the targeted longer-term refinancing operations, the Governing Council will regularly assess how targeted lending operations and their ongoing repayment are contributing to its monetary policy stance.

資料來源: 中央社