- 美國聯準會9月20日決策會議決議維持利率不變,指標聯邦基金利率區間仍然是5.25%~5.5%,是2001年以來的新高水準

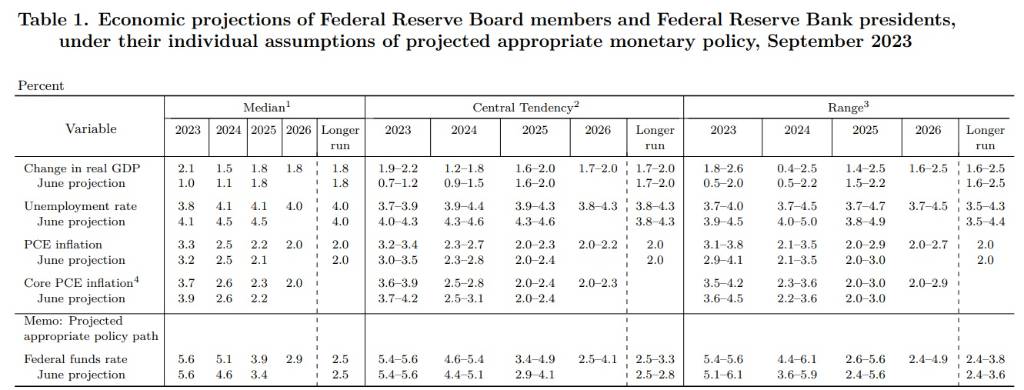

- 這次決策會議公布的經濟展望,預估2023年聯邦基金利率中值為5.6%,比目前利率水準高1碼(0.25%)

- 預估2024年聯邦基金利率中值為5.1%,相較2023年預估值下降0.5%,顯示2024年仍然有降息可能性

美國聯準會9月20日決策會議決議維持利率不變,指標聯邦基金利率區間仍然是5.25%~5.5%,是2001年之後22年來的新高水準。

回顧聯準會自2022年3月16日展開這波升息循環,共計升息11次(2022年7次共17碼+2023年4次共4碼),累計升幅達21碼(5.25%),這11次升息的宣布時間與升息幅度,依序為2022年3月16日升息1碼、2022年5月4日升息2碼、2022年6月15日升息3碼、2022年7月27日升息3碼、2022年9月21日升息3碼、2022年11月2日升息3碼,2022年12月15日升息2碼,2023年2月1日升息1碼,2023年3月22日升息1碼,2023年5月3日升息1碼,2023年7月26日升息1碼。

聯準會在聲明中表示,最近的經濟指標顯示經濟活動一直在穩定擴張,近幾個月就業成長放緩,但仍保持強勁,失業率維持在相對較低的水準,通貨膨脹率仍然居高不下。美國銀行體系健全且富有彈性,家庭與企業信貸條件縮緊可能會對經濟活動、就業、通膨產生壓力,這些影響的程度仍有不確定性,委員會仍然高度關注通膨風險。

委員會力求長期達到最大就業與達到通膨率2%的目標,為支持這個目標決議維持利率在5.25%~5.5%,之後將會繼續評估更多資訊,及對貨幣政策的影響。委員會將考慮貨幣政策的累積緊縮,貨幣政策影響經濟活動與通膨的延遲性,與金融、經濟狀況。

關於縮減資產負債表(縮表/QT)的行動計劃,維持公債每月縮減上限600億美元,抵押貸款證券(MBS)每月縮減上限350億美元。

這次決策會議公布的經濟展望

- 預估2023年實質國內生產毛額(GDP)成長率為2.1%,相較6月的預估值上修1.1%;預估2024年實質GDP成長率為1.5%,相較6月的預估值上修0.4%。

- 預估2023年失業率為3.8%,相較6月的預估值下修0.3%;預估2023年失業率為4.1%,相較6月的預估值下修0.4%。

- 預估2023年個人消費支出(PCE)物價指數成長率為3.3%,相較6月的預估值上修0.1%;預估2024年PCE物價指數成長率為2.5%,與6月的預估值相同。預估2023年核心PCE物價指數成長率為3.7%,相較6月的預估值下修0.2%;預估2024年核心PCE物價指數成長率為2.6%,與6月的預估值相同。預估2023年~2025年核心PCE物價指數成長率都會大於整體PCE物價指數成長率,顯示近3年服務類的通膨率可能都會大於商品類的通膨率。

- 預估2023年聯邦基金利率中值為5.6%,與6月的預估值相同;預估2024年聯邦基金利率中值為5.1%,相較6月的預估值上修0.5%。2024年聯邦基金利率中值相較2023年預估值下降0.5%,顯示2024年仍然有降息可能性。

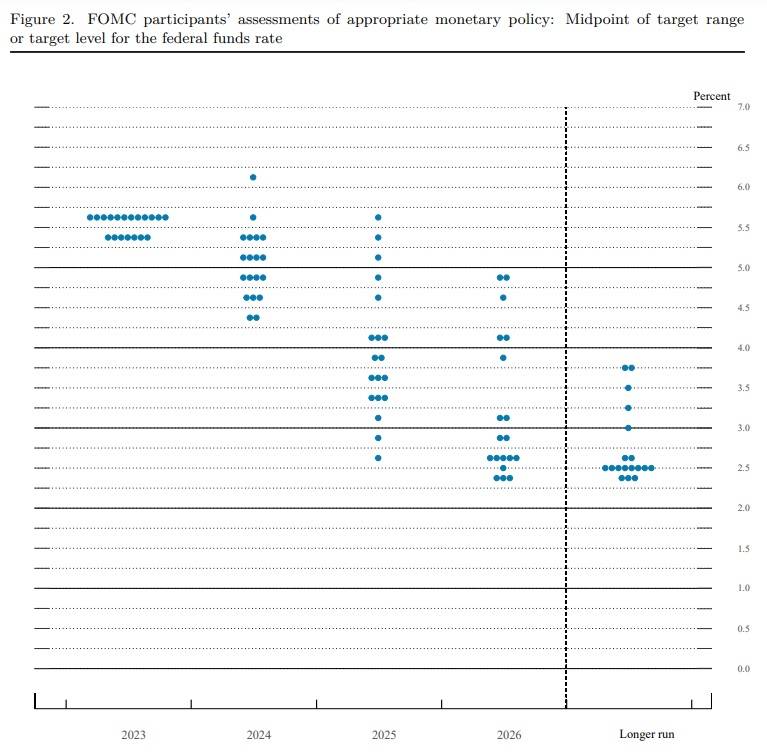

這次會議公布的點陣圖當中,19位委員當中,12位(63%)預期2023年聯邦基金利率區間位於5.5%~5.75%,與目前5.25%~5.5%的水準相較,仍保有升息1碼(0.25%)的空間;13位(68%)預期2024年聯邦基金利率區間會在5%~5.25%以下,與目前5.25%~5.5%的水準相較,有降息1碼以上的可能性。

圖資來源:美國聯準會

Federal Reserve issues FOMC statement (September 20, 2023)

Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have slowed in recent months but remain strong, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. The Committee will continue to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Implementation Note issued September 20, 2023

Decisions Regarding Monetary Policy Implementation

The Federal Reserve has made the following decisions to implement the monetary policy stance announced by the Federal Open Market Committee in its statement on September 20, 2023:

- The Board of Governors of the Federal Reserve System voted unanimously to maintain the interest rate paid on reserve balances at 5.4 percent, effective September 21, 2023.

- As part of its policy decision, the Federal Open Market Committee voted to direct the Open Market Desk at the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the System Open Market Account in accordance with the following domestic policy directive:

"Effective September 21, 2023, the Federal Open Market Committee directs the Desk to:

- Undertake open market operations as necessary to maintain the federal funds rate in a target range of 5-1/4 to 5-1/2 percent.

- Conduct standing overnight repurchase agreement operations with a minimum bid rate of 5.5 percent and with an aggregate operation limit of $500 billion.

- Conduct standing overnight reverse repurchase agreement operations at an offering rate of 5.3 percent and with a per-counterparty limit of $160 billion per day.

- Roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing in each calendar month that exceeds a cap of $60 billion per month. Redeem Treasury coupon securities up to this monthly cap and Treasury bills to the extent that coupon principal payments are less than the monthly cap.

- Reinvest into agency mortgage-backed securities (MBS) the amount of principal payments from the Federal Reserve's holdings of agency debt and agency MBS received in each calendar month that exceeds a cap of $35 billion per month.

- Allow modest deviations from stated amounts for reinvestments, if needed for operational reasons.

- Engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency MBS transactions."

- In a related action, the Board of Governors of the Federal Reserve System voted unanimously to approve the establishment of the primary credit rate at the existing level of 5.5 percent.

This information will be updated as appropriate to reflect decisions of the Federal Open Market Committee or the Board of Governors regarding details of the Federal Reserve's operational tools and approach used to implement monetary policy.

資料來源: 經濟日報