- 聯準會於6月18日決議維持聯邦資金利率於4.25%至4.50%不變,此舉獲全體成員一致通過

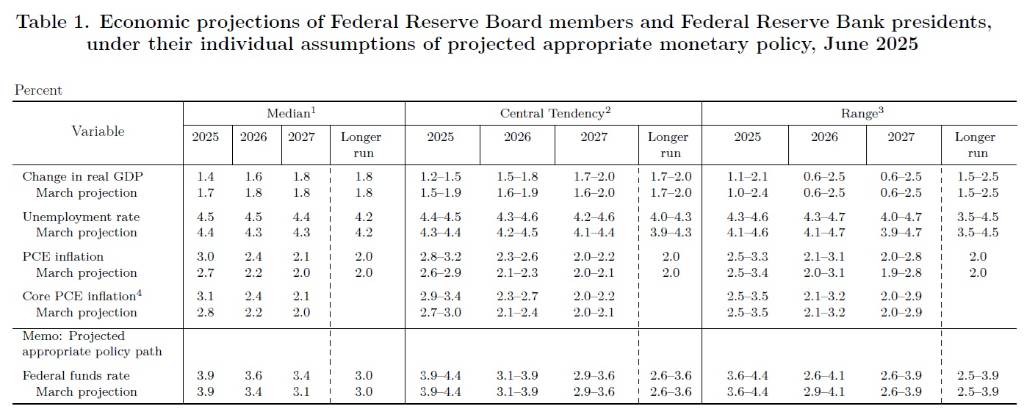

- 聯準會下修2025年GDP成長率預估至1.4%,並上修同年整體PCE通膨率至3.0%,核心PCE為3.1%

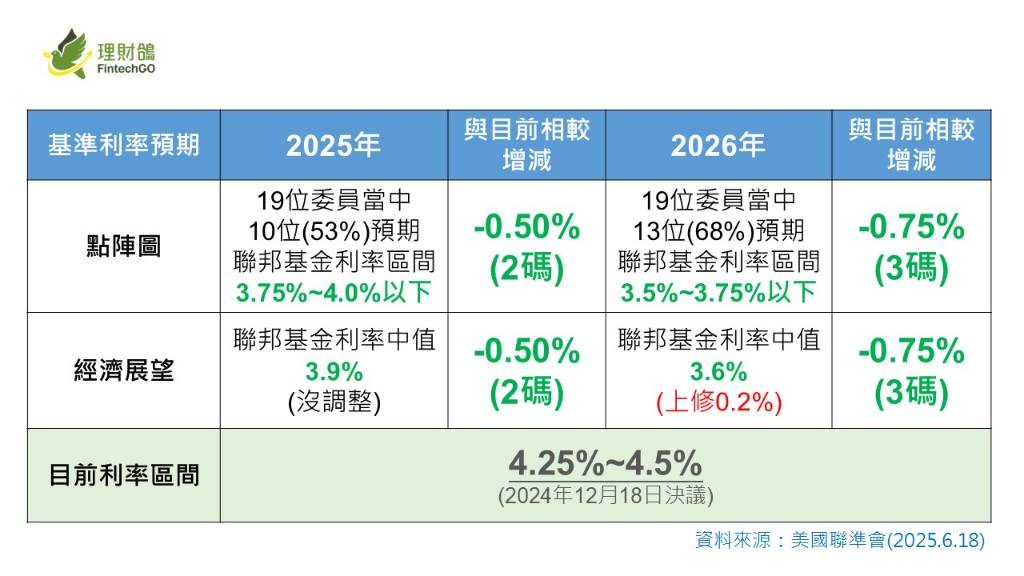

- 儘管利率維持不變,聯準會點陣圖預示2025年稍晚可能降息2次,2026年與2027年各降息1碼

聯準會(Fed)於2025年6月18日召開的聯邦公開市場委員會(FOMC)會議上,決議維持其政策利率,即聯邦資金利率目標區間在4.25%至4.50%不變。儘管面對經濟前景的不確定性,委員會認為當前的貨幣政策立場有助於及時應對潛在的經濟發展。此外,聯準會也將持續縮減其資產負債表規模。此政策決定獲得全體委員會成員一致贊成。

聯準會主席鮑威爾表示,聯準會的首要任務是實現充分就業與穩定物價的雙重使命。他指出,儘管不確定性升高,美國經濟仍處於穩健狀態。美國失業率維持在低點,勞動市場正處於或接近充分就業水平。近三個月,美國平均每月非農就業人口增加13.5萬人。失業率為4.2%,過去一年來維持在窄幅區間內。薪資成長持續趨緩,但仍超過通膨速度。整體而言,多項指標顯示勞動市場趨於平衡,且並非造成顯著通膨壓力的來源。

在經濟活動方面,美國經濟整體持續以穩健速度擴張。去年經濟成長率為2.5%。今年第一季國內生產毛額(GDP)略微下滑,主因是企業為規避潛在關稅而提前進口所造成的淨出口波動。然而,排除淨出口、存貨投資和政府支出的私人國內最終購買量(PDFP)則以2.5%的穩健速度成長。

鮑威爾指出,雖然通膨已從2022年中期的歷史高點顯著下降,但仍略高於聯準會設定的2.0%長期目標。根據消費者物價指數(CPI)及其他數據估計,截至今年5月的12個月期間,整體個人消費支出(PCE)物價指數年增率為2.3%。排除波動較大的食品與能源價格後,核心PCE物價指數年增率則達2.6%。近期通膨預期在最近幾個月有所上升,這反映在市場和調查數據中。消費者、企業和專業預測人士的調查結果皆指出,關稅是主要的推升因素。然而,展望未來一年左右,多數長期通膨預期仍與2.0%的目標一致。

聯準會官員透過最新的經濟預測摘要(SEP)顯示,對未來經濟展望進行修正。2025年經濟成長率預估中值下修至1.4%,較3月預測的1.7%下降0.3%。2026年GDP成長率預估中值為1.6%,相較3月預測的1.8%下修0.2%。

通膨預期則普遍上修。2025年整體PCE通膨率預估中值為3.0%,較3月預測的2.7%上修0.3%。核心PCE通膨率預估中值亦上修至3.1%,較3月預測的2.8%上修0.3%。儘管2026年和2027年通膨預估中值將分別回落至2.4%和2.1%,但仍略高於3月預測。失業率方面,2025年底的失業率預估中值上修至4.5%,較3月預測的4.4%增加0.1%。這也比目前4.2%的實際水準高出0.3%。

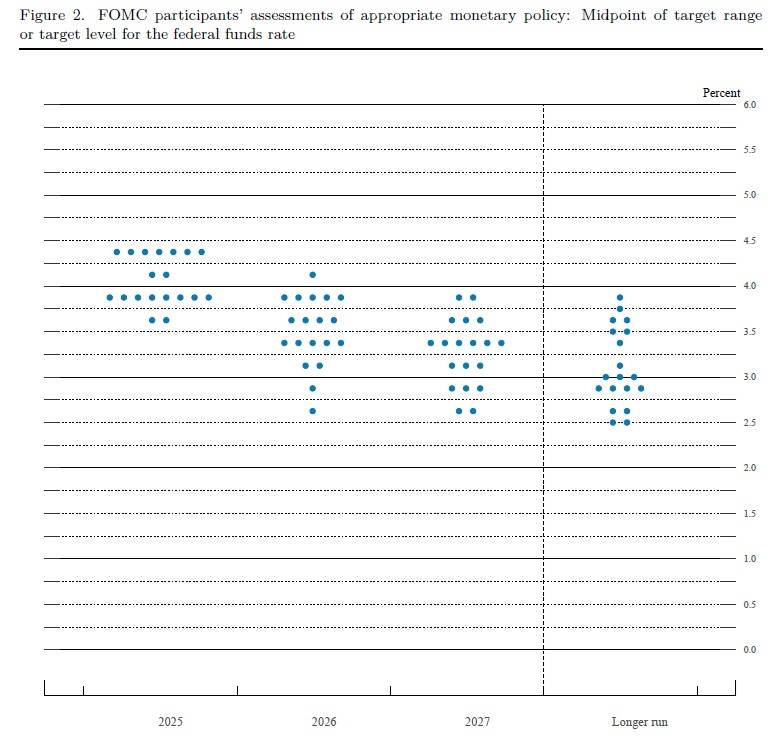

聯邦公開市場委員會(FOMC)參與者對未來聯邦資金利率的適當路徑進行個人評估。預計2025年底聯邦資金利率中值為3.9%,與3月預測相同。此中值暗示今年稍晚可能進行兩次降息。預計2026年底將進一步降至3.6%,2027年底則降至3.4%,兩者皆略高於3月預測。委員會成員對利率走勢的看法存在高度不確定性,從「點陣圖」(dot plot)中可以看出其分佈範圍相當分散。在19位與會官員中,有7人認為今年不應降息,這一數字高於3月時的4人。鮑威爾強調,這些個人預測並非委員會的計畫或決定,且當前的不確定性異常高。

聯準會將根據未來經濟數據、不斷演變的經濟前景以及風險平衡來決定貨幣政策的適當立場。主席鮑威爾指出,貿易、移民、財政和監管政策的變化持續演變,其對經濟的影響仍不確定。雖然對貿易政策不確定性的擔憂有所減少,但整體經濟前景的不確定性依然偏高。預計今年關稅的增加可能會推高物價並抑制經濟活動。他強調,聯準會的義務是保持長期通膨預期穩定,並防止一次性的物價上漲演變成持續的通膨問題。

鮑威爾承認,聯準會可能面臨其雙重使命目標,充分就業與穩定物價,處於緊張狀態的挑戰情境。若發生此情況,委員會將會權衡經濟與每個目標的距離,以及預計彌補這些差距所需的潛在不同時間範圍。就目前而言,聯準會處於有利位置,可以等待進一步了解經濟可能走向後,再考慮調整政策立場。

Federal Reserve issues FOMC statement (June 18, 2025)

Although swings in net exports have affected the data, recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook has diminished but remains elevated. The Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Austan D. Goolsbee; Philip N. Jefferson; Adriana D. Kugler; Alberto G. Musalem; Jeffrey R. Schmid; and Christopher J. Waller.

Implementation Note issued June 18, 2025

Decisions Regarding Monetary Policy Implementation

The Federal Reserve has made the following decisions to implement the monetary policy stance announced by the Federal Open Market Committee in its statement on June 18, 2025:

- The Board of Governors of the Federal Reserve System voted unanimously to maintain the interest rate paid on reserve balances at 4.4 percent, effective June 20, 2025.

- As part of its policy decision, the Federal Open Market Committee voted to direct the Open Market Desk at the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the System Open Market Account in accordance with the following domestic policy directive:

"Effective June 20, 2025, the Federal Open Market Committee directs the Desk to:

- Undertake open market operations as necessary to maintain the federal funds rate in a target range of 4-1/4 to 4‑1/2 percent.

- Conduct standing overnight repurchase agreement operations with a minimum bid rate of 4.5 percent and with an aggregate operation limit of $500 billion.

- Conduct standing overnight reverse repurchase agreement operations at an offering rate of 4.25 percent and with a per‑counterparty limit of $160 billion per day.

- Roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing in each calendar month that exceeds a cap of $5 billion per month. Redeem Treasury coupon securities up to this monthly cap and Treasury bills to the extent that coupon principal payments are less than the monthly cap.

- Reinvest the amount of principal payments from the Federal Reserve's holdings of agency debt and agency mortgage‑backed securities (MBS) received in each calendar month that exceeds a cap of $35 billion per month into Treasury securities to roughly match the maturity composition of Treasury securities outstanding.

- Allow modest deviations from stated amounts for reinvestments, if needed for operational reasons."

- In a related action, the Board of Governors of the Federal Reserve System voted unanimously to approve the establishment of the primary credit rate at the existing level of 4.5 percent.

This information will be updated as appropriate to reflect decisions of the Federal Open Market Committee or the Board of Governors regarding details of the Federal Reserve's operational tools and approach used to implement monetary policy.

圖資來源:聯準會

資料來源: 鉅亨網